Trade Secrets: Dailies 02.05.2026

US stock futures edged higher late Wednesday as investors digested another batch of corporate earnings and assessed fresh signals from Alphabet, following a sharp sell-off that hit technology stocks earlier in the day.

- US stock futures edged higher late Wednesday as investors digested another batch of corporate earnings and assessed fresh signals from Alphabet, following a sharp sell-off that hit technology stocks earlier in the day.

- Alphabet (GOOG) shares slipped more than 1% in late trading after the company reported results and outlined a significant ramp-up in artificial intelligence investment. The Google parent said it expects expenditure to climb, projecting spending as high as $185 billion in 2026. But that outlook helped lift shares of tech names such as Nvidia (NVDA) and Broadcom (AVGO), as investors renewed optimism around long-term demand tied to AI infrastructure.

- Elsewhere, Qualcomm (QCOM) shares tumbled nearly 9% after the chipmaker issued a softer-than-expected forecast, citing headwinds from a global memory shortage.

- Software names bore the brunt of a decline Wednesday as Anthropic AI tools led to fears of disruption in traditional business models. Crypto markets were also rattled following a comment from Treasury Secretary Scott Bessent, who said the government would not bail out bitcoin (BTC-USD) amid an over 13% drop over the past five days that has pushed the token to around $73,000.

- Looking ahead, earnings remain in focus, with Amazon (AMZN) taking focus Thursday. Investors will also be watching weekly jobless claims data due in the morning for fresh clues on the health of the labor market.

- Asian stock markets fell on Thursday, retreating from record highs hit earlier in the week, as sharp volatility in global technology shares amid AI disruption worries weighed on investor sentiment.

- The pullback followed a sharp sell-off in U.S. technology stocks overnight, where the Nasdaq fell more than broader benchmarks.

- The downturn comes after a turbulent week for technology and semiconductor stocks, driven by growing concerns that rapid advances in artificial intelligence could disrupt existing business models and compress margins, prompting investors to take profits after a strong rally.

- South Korea’s benchmark index KOSPI dropped 3.7% after surging to record highs over the previous two sessions. Shares of Samsung Electronics (KS:005930) and SK Hynix (KS:000660) fell over 5% each as investors locked in profits following the recent rally.

- China's blue chip Shanghai Shenzhen CSI 300 index and the Shanghai Composite index fell nearly 1% each.

- Hong Kong's Hang Seng slipped 1.2%, with the Hang Seng TECH sub-index losing 1.5%.

- In Japan, the Nikkei 225 fell 1%, easing from record highs reached earlier this week, as technology stocks tracked overnight losses on Wall Street.

- Nikkei's losses was capped by strong gains in select names, with Panasonic (TYO:6752) surging after reporting robust earnings and upbeat guidance, while Renesas Electronics (TYO:6723) jumped after announcing the sale of its timing business to U.S.-based SiTime in a deal valued at about $3 billion.

- The broader TOPIX index traded largely flat, reflecting relative resilience outside the technology sector.

- Singapore’s Straits Times Index edged 0.4% lower after closing at a record high in the previous session.

- Australia's S&P/ASX 200 index also fell 0.4%, tracking regional losses, as investors digested trade data released earlier in the day.

- Australia’s trade surplus widened less than expected in December, reflecting subdued export growth alongside softer imports, reinforcing concerns that global demand remains uneven.

- Futures tied to India's Nifty 50 inched down 0.3%.

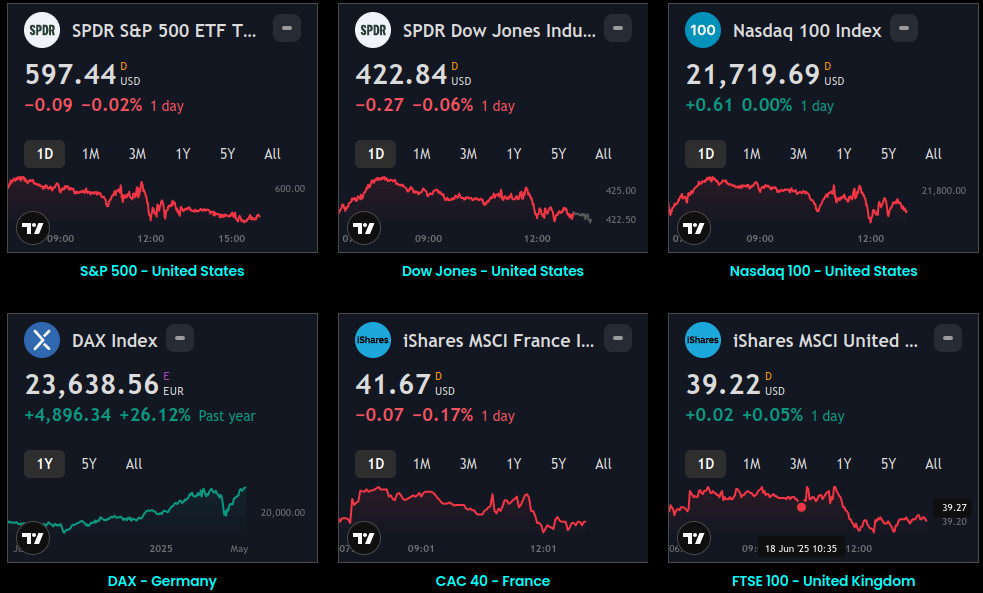

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.