- US stock futures slid after an upbeat day on Wall Street as investors parse the final leg of President Trump’s meeting with Chinese President Xi Jinping.

- After markets closed, shares of Applied Materials (AMAT) and Figma (FIG) jumped as investors cheered earnings results that signaled strong demand amid the AI boom.

- In day trading, the Dow (^DJI) jumped back to the 50,000 level, and the S&P 500 (^GSPC) and Nasdaq (^IXIC) hit new highs, powered by confidence in the AI trade. President Trump’s summit with Chinese President Xi Jinping and the blockbuster market debut of chipmaker Cerebras (CBRS) also lifted market sentiment.

- Trump is currently concluding his visit with Xi in Beijing before heading back to Washington. So far, his visit has struck a business-friendly tone, with 16 top US executives accompanying him, and as of Thursday, new deals for the likes of Boeing (BA) and Nvidia (NVDA). The diplomatic issues of Taiwan and Iran, however, continue to lurk in the background.

- Earnings season continues to wrap up this week, with Mizuho Financial Group (MFG), RBC Bearings (RBC), and Sigma Lithium Corporation (SGML) posting results Friday.

- Most Asian stocks fell on Friday as chipmaking stocks were pressured by doubts over the U.S. allowing more sales to China, with focus remaining squarely on an ongoing summit in Beijing.

- Chinese markets steadied near multi-year highs as markets sought more details on talks between President Xi Jinping and U.S. President Donald Trump.

- South Korean stocks were the worst performers, falling sharply after a U.S. trade official said U.S. chip export controls were not discussed in detail during recent talks.

- Asian markets largely brushed off a positive lead-in from Wall Street, which hit record highs on Thursday as reports of the U.S. allowing more chip sales to China boosted tech stocks.

- South Korea’s KOSPI was by far the worst performer in Asia on Friday, falling 3.5% on steep losses in major chipmaking stocks.

- Other Asian chipmakers also fell, with Japan’s Tokyo Electron Ltd. (TYO:8035) and Advantest Corp. (TYO:6857) losing between 1% and 6%.

- U.S. Trade Representative Jamieson Greer told Bloomberg that Thursday’s U.S.-China talks did not discuss chip export controls, and that it was up to Beijing to decide on whether it wanted to buy U.S. chips.

- Greer’s comments largely overshadowed a Thursday report which said NVIDIA Corporation (NASDAQ:NVDA) was allowed to sell its H200 chip to 10 Chinese companies. While the report did note that no actual sales were made so far, chipmaking stocks rallied sharply on Thursday.

- China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes were flat, remaining close to their respective 4-½ year and 11-year highs hit earlier this week.

- Focus was squarely on more talks between Trump and Xi, scheduled for later on Friday. The two had met on Thursday and had flagged hopes for improving relations between the world’s biggest economies.

- Trump claimed in a Fox News interview that China had agreed to buy U.S. oil, and had also agreed to purchase more Boeing jets. Separately, China’s foreign ministry said Trump and Xi had reached consensus on several topics, although details remained unclear.

- Broader Asian markets mostly fell, with Japan also coming under pressure from a hot inflation reading.

- Japan’s Nikkei 225 index slid 1.6%, while the TOPIX lost 0.3% after data showed producer price index inflation blew past estimates in April. The print was largely driven by higher oil and chemical prices stemming from the Iran conflict, and pointed to a broader increase in Japanese inflation, which could elicit an interest rate hike from the Bank of Japan.

- Hong Kong’s Hang Seng index fell 1% on losses in local tech shares, while Singapore’s Straits Times index shed 0.1%.

- Australia’s ASX 200 was flat, while India’s Nifty 50 index added 0.4% in early trade.

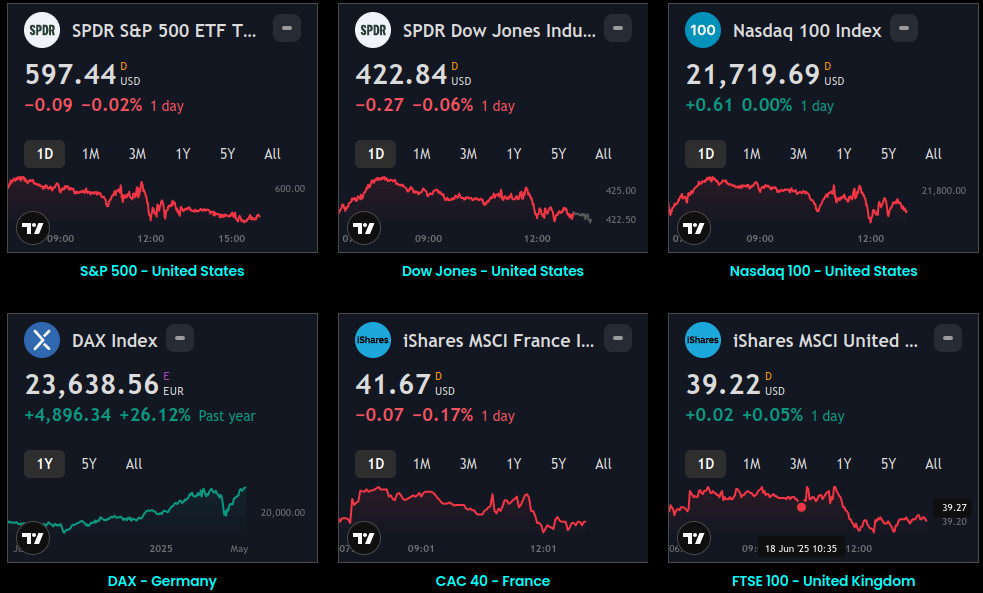

Global Indices:

Global Indices Dashboard

S&P 500 - United States Dow Jones - United States Nasdaq 100 - United States DAX - Germany CAC 40 - France FTSE 100 - United Kingdom Nikkei 225 - Japan EWH - Hong Kong Sensex - India ASX 200 - Australia MOEX - Russia MERVAL - Argentina Bovespa

Active Stocks:

Active Stocks

See the top five gaining, losing, and most active stocks for the day. It updates based on current market activity – so you’ll always see the most relevant stocks Track all markets on TradingView

Stocks, ETFs and Funds Screener:

Stocks, ETFs and Funds

Separate the wheat from the chaff – handy for sorting symbols both by fundamental and technical indicators. Sort Assets and Filter by Region, Type, Sector, Industry and Country

Forex:

Foreign Exchange Dashboard

Heatmap and Real-time quotes of selected currencies in comparison to other major currencies. Sort currencies both by fundamental and technical indicators

CryptoCurrency:

Crypto Currency Dashboard

CRYPTO HEATMAP OVERVIEW Assets by Market Capitalization

Events and Earnings Calendar:

Events & Earnings

Keep an eye on key upcoming economic events, announcements, and news. Track all markets on TradingView

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.