- US stock futures cautiously rose as the world awaited an update on US-Iran peace talks.

- Stocks rebounded on Thursday after Secretary of State Marco Rubio and Iranian media signaled progress on negotiations between the US and Iran for a peace deal.

- Markets started the week on a down note, with concerns of persistent inflation stoking worries about Federal Reserve rate hikes. Since reports of movement on US-Iran talks picked up on Wednesday, however, investors have had reason to believe a primary source of rising prices could be resolved soon.

- On Friday, the University of Michigan’s latest readings on consumer sentiment and inflation expectations will offer fresh insight into how much price pressures are rising as the war drags on.

- Earnings season also continues to wrap up, with major government contractor Booz Allen Hamilton (BAH) reporting its results before the bell.

- Asian stock markets extended gains on Friday and headed for weekly advances as chipmakers rebounded after upbeat earnings from Nvidia, while unresolved issues in U.S.-Iran negotiations kept investors cautious.

- Wall Street had closed slightly higher overnight, with the Dow Jones Industrial Average marking a record close.

- Investors piled back into chipmakers after Nvidia’s strong outlook underscored resilient spending on AI infrastructure.

- Japan’s Nikkei 225 jumped more than 2.5% to hover near record highs, set to climb nearly 3% for the week.

- Japan's broader TOPIX index rose nearly 1%.

- Japanese technology investor SoftBank Group (TYO:9984) extended sharp gains on optimism over a potential OpenAI initial public offering and expectations that Arm Holdings will benefit from booming AI demand.

- China's Shanghai Composite index rose 0.5%, while Hong Kong's Hang Seng climbed 1.3%.

- South Korea’s KOSPI edged 0.2% higher, heading for a 4.5% weekly jump.

- Samsung Electronics (KS:005930) shares fell about 2% on Friday as union workers began voting on a tentative pay agreement reached earlier this week that narrowly averted a potentially damaging 18-day strike involving tens of thousands of employees.

- Samsung shares had jumped 9% on Thursday after the tentative agreement led to the suspension of strike action.

- Still, gains across the region were capped by lingering uncertainty surrounding negotiations between Washington and Tehran.

- Officials on both sides pointed to signs of progress, but disagreements remained over Iran’s uranium stockpile and proposed controls in the Strait of Hormuz, a vital route for global oil shipments.

- U.S. Secretary of State Marco Rubio said there were “some good signs” in the talks but rejected any proposal involving tolls for ships using the strait.

- Oil prices rebounded after a sharp decline in the previous session as doubts resurfaced over whether the talks would ultimately produce a lasting agreement. Higher crude prices continued to fuel worries over inflation and global interest rates.

- India's Nifty 50 and Singapore's Straits Times Index rose 0.4% each.

- Australia's S&P/ASX 200 gained 0.5%.

- In Japan, data on Friday showed core consumer inflation slowed to a four-year low of 1.4% in April, easing from 1.8% in March and missing market forecasts, largely due to government fuel subsidies and lower education costs.

- However, analysts expect inflation pressures to rebound in coming months as higher energy prices linked to Middle East tensions feed through the economy.

- The inflation data did little to alter expectations that the Bank of Japan could still raise interest rates later this year, with some investors even betting on a possible June move as surging oil costs and a weak yen threaten to push prices higher again.

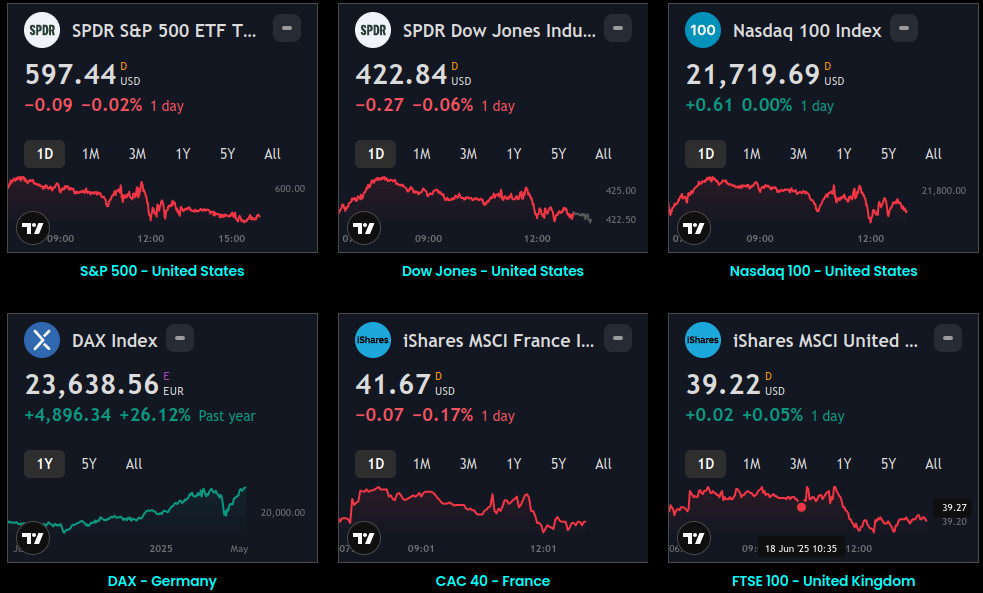

Global Indices:

Global Indices Dashboard

S&P 500 - United States Dow Jones - United States Nasdaq 100 - United States DAX - Germany CAC 40 - France FTSE 100 - United Kingdom Nikkei 225 - Japan EWH - Hong Kong Sensex - India ASX 200 - Australia MOEX - Russia MERVAL - Argentina Bovespa

US Stocks lowered as Wall Street awaited Nvidia earnings, hoping strong results could offer some relief from ongoing inflation concerns.Active Stocks:

Active Stocks

See the top five gaining, losing, and most active stocks for the day. It updates based on current market activity – so you’ll always see the most relevant stocks Track all markets on TradingView

Stocks, ETFs and Funds Screener:

Stocks, ETFs and Funds

Separate the wheat from the chaff – handy for sorting symbols both by fundamental and technical indicators. Sort Assets and Filter by Region, Type, Sector, Industry and Country

Forex:

Foreign Exchange Dashboard

Heatmap and Real-time quotes of selected currencies in comparison to other major currencies. Sort currencies both by fundamental and technical indicators

CryptoCurrency:

Crypto Currency Dashboard

CRYPTO HEATMAP OVERVIEW Assets by Market Capitalization

Events and Earnings Calendar:

Events & Earnings

Keep an eye on key upcoming economic events, announcements, and news. Track all markets on TradingView

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.