- US stock futures traded mixed on Monday morning after Iran attacked Israel, putting pressure on a fragile ceasefire in the Middle East, and investors continued to reprice rate-hike bets and assess the artificial intelligence trade.

- Markets start the week on unsteady footing after the Nasdaq Composite (^IXIC) dropped 4% on Friday and the S&P 500 (^GSPC) snapped its nine-week winning streak. A strong rotation out of high-flying semiconductor stocks and into more defensive areas of the market came on the heels of a blowout May jobs report that strengthened the case for the Federal Reserve to raise interest rates later this year.

- The Nasdaq eyed a rebound on Monday as Nvidia (NVDA) CEO Jensen Huang and others suggested the tech rout could be an opportunity to buy into the AI trade. Chip stocks gained in premarket, with Micron (MU) up 4% and Nvidia adding nearly 2%.

- Oil prices flared after Iran fired missiles at Israel for the first time since April, and Israel struck back despite President Trump's calls for both sides to stop fighting. Brent futures (BZ=F) climbed over 4% to almost $97 a barrel, while West Texas Intermediate futures (CL=F) neared $95 a barrel amid revived concerns that a US ceasefire with Iran could fall apart to return open conflict in the Middle East.

- Investors will get a better sense of whether higher oil prices are starting to bleed into core prices on Wednesday with the release of the latest monthly Consumer Price Index. That's followed by an update on the Fed's preferred gauge of inflation, the Producer Price Index, on Thursday. The Fed's focus will be squarely on inflation after a batch of jobs data last week showed the labor market remains stable.

- Other key events to watch this week include Oracle (ORCL) earnings on Wednesday and the likely SpaceX (SPCX) IPO on Friday, which is expected to be the largest public offering on record.

- Asian stocks fell sharply on Monday with technology and artificial intelligence stocks leading declines as investors collected big profits from a major rally in the sector, while worsening military tensions in the Middle East also weighed.

- South Korea’s KOSPI was by far the worst performer in the region on deep losses in heavyweight chipmaking stocks, while Japan’s Nikkei 225 also tumbled on tech losses.

- Regional markets took an extremely weak lead-in from Wall Street’s close on Friday, where major benchmarks tumbled between 1% and 4.5%. Tech was the biggest decliner, with a hotter-than-expected nonfarm payrolls reading also driving up expectations for interest rate hikes.

- But S&P 500 Futures and Nasdaq 100 Futures rose 0.2% and 0.7%, respectively, in Asian trade, with investors looking to a potential rebound in U.S. tech shares from Friday’s slump.

- South Korea’s KOSPI index was by far the worst performer in Asia, tumbling as much as 8.8% on sharp losses in local chip heavyweights.

- Samsung Electronics Co Ltd (KS:005930) and SK Hynix Inc (KS:000660)– the two memory chip makers that had driven a bulk of the KOSPI’s recent gains– fell 4.7% and 1.1%, respectively. SK Hynix’s losses were limited by the company announcing an advanced chips tie-up with AI major NVIDIA Corporation (NASDAQ:NVDA).

- Gains in tech saw the KOSPI largely outpace global stock markets so far this year, although this also left the sector vulnerable to profit-taking.

- Japan’s Nikkei 225 index slid 3.6%, pressured chiefly by losses in local tech majors as investors questioned whether the AI tech rally had gone too far.

- Tech major SoftBank Group Corp. (TYO:9984) slid 7.5% and was among the biggest weights on the Nikkei, while chipmaking majors including SUMCO Corp. (TYO:3436) and Renesas Electronics Corp (TYO:6723) slid over 10% each.

- Japan’s broader TOPIX index slid 2.7%, also spooked by a downward revision in the country’s gross domestic product figures for the first quarter.

- Japan’s economy grew 1.8% in the first quarter, lower than prior estimates of 2.1%, pressured chiefly by cooling business spending, data showed on Monday.

- The print raised some questions over the impact of the Iran war on growth, and also saw investors questioning whether the Bank of Japan will have enough headroom to raise interest rates next week.

- Beyond tech, broader Asian markets fell on Monday after Iran and Israel traded airstrikes on Sunday, marking their first open exchange of hostilities since an early-April ceasefire.

- The development further undermined hopes for a lasting peace deal with Iran, even as U.S. President Donald Trump and other officials said an agreement was close. Trump had earlier on Sunday also called on Israel to not retaliate against Iranian strikes over the weekend, citing progress towards a peace deal.

- Oil prices rose sharply on the weekend development, further spooking Asian markets. China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes fell 1.6% and 1.2%, respectively, while Hong Kong’s Hang Seng shed 1%.

- Singapore’s Straits Times index fell 1.2%. Futures for India’s Nifty 50 index rose 0.3% after the Nifty logged deep losses last week.

- Beyond geopolitics, Asian markets were also spooked by a strong U.S. nonfarm payrolls reading on Friday. Strength in jobs gives the Federal Reserve more headroom to maintain rates or even raise them– a trend that bodes poorly for risk-driven markets.

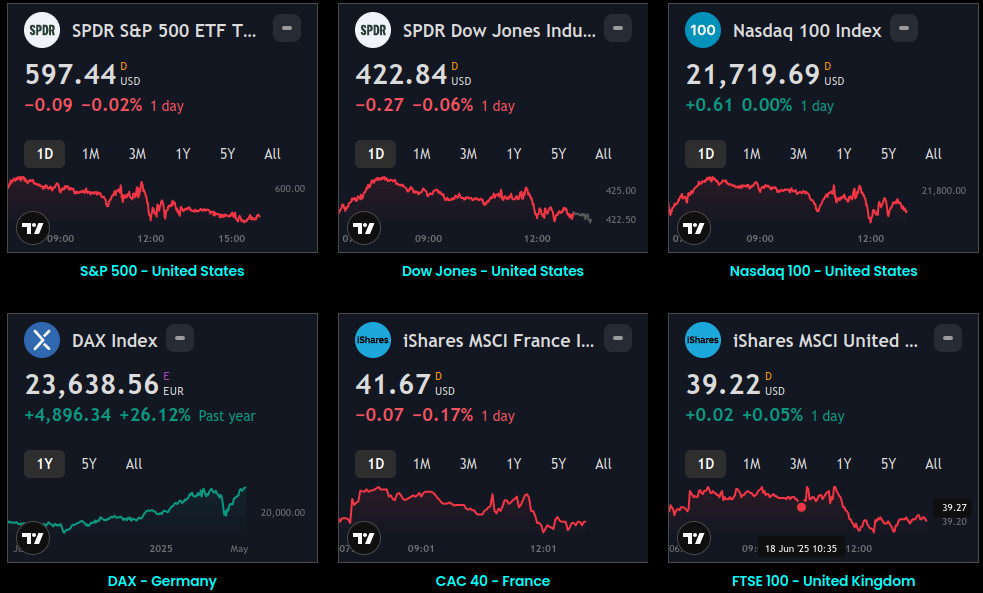

Global Indices:

Global Indices Dashboard

S&P 500 - United States Dow Jones - United States Nasdaq 100 - United States DAX - Germany CAC 40 - France FTSE 100 - United Kingdom Nikkei 225 - Japan EWH - Hong Kong Sensex - India ASX 200 - Australia MOEX - Russia MERVAL - Argentina Bovespa

Active Stocks:

Active Stocks

See the top five gaining, losing, and most active stocks for the day. It updates based on current market activity – so you’ll always see the most relevant stocks Track all markets on TradingView

Stocks, ETFs and Funds Screener:

Stocks, ETFs and Funds

Separate the wheat from the chaff – handy for sorting symbols both by fundamental and technical indicators. Sort Assets and Filter by Region, Type, Sector, Industry and Country

Forex:

Foreign Exchange Dashboard

Heatmap and Real-time quotes of selected currencies in comparison to other major currencies. Sort currencies both by fundamental and technical indicators

CryptoCurrency:

Crypto Currency Dashboard

CRYPTO HEATMAP OVERVIEW Assets by Market Capitalization

Events and Earnings Calendar:

Events & Earnings

Keep an eye on key upcoming economic events, announcements, and news. Track all markets on TradingView

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.