US Stocks hold near highs as markets digest Monday's Iran peace deal surge, with attention now squarely on the Federal Reserve's first meeting under new chairman Kevin Warsh beginning today, and a pair of blockbuster deal announcements dominating the premarket tape.

- SpaceX (SPCX) is the story of the premarket, surging 8.9% to above $200 per share — adding nearly $1 trillion in market cap in just four days since its $135 IPO price — after the company announced a $60 billion all-stock deal to acquire Anysphere, the San Francisco startup behind AI coding assistant Cursor. The deal, structured as a merger between Anysphere and SpaceX subsidiary X67 Inc., is expected to close in Q3 2026. Before SpaceX came knocking, Cursor was on track to close a $2 billion funding round at a $50 billion valuation. The acquisition is designed to strengthen SpaceX's AI division — built around its February merger with Elon Musk's xAI — in the enterprise AI coding market where rivals OpenAI and Anthropic have found early commercial traction. SpaceX carries $2.4 trillion and $22.7 trillion addressable market ambitions in AI infrastructure and enterprise applications respectively per its IPO filing.

- Yum! Brands (YUM) announced it is selling Pizza Hut for $2.7 billion in total — $1.5 billion to private equity firm LongRange Capital for all operations outside mainland China, and $1.2 billion to Yum China Holdings for mainland China locations — ending 47 years of ownership of the brand. The sale follows a strategic review begun in November 2025 after years of U.S. same-store sales declines of 4–5% annually and a shrinking domestic unit count. Yum approved a $4 billion incremental share repurchase. Shares rose 0.85% in premarket.

- Tripadvisor (TRIP) jumped 12% in premarket after American Express said it will acquire restaurant booking platform TheFork from the online travel company in an all-cash deal worth $700 million, with the transaction expected to close in Q3 2026.

- On the Iran front, the peace deal announced Sunday remains intact but new complications have emerged around Lebanon. Trump criticized Netanyahu on Tuesday over Israel's continued operations against Hezbollah in Lebanon, telling CBS News that the parallel fighting was complicating his efforts to finalize the broader agreement with Iran. Iran's foreign minister warned that any continued Israeli military presence in southern Lebanon, or further strikes there, would constitute a violation of the emerging U.S.-Iran understanding. Israeli officials said troops would remain in Lebanon regardless, creating a new source of friction ahead of Friday's formal Switzerland signing ceremony.

- Oil prices extended their decline, with Brent crude edging down further after Monday's 4–5% drop, now trading near $83 per barrel. Gold futures edged up 0.38% to $4,368.30 and silver gained 0.51% to $70.54, supported by continued dollar weakness.

- The week's central macro event begins today as the Federal Reserve opens its two-day June 16–17 FOMC meeting — Kevin Warsh's first as chair. The rate is widely expected to hold at 3.50%–3.75%, but markets are watching for whether Warsh scraps the dot plot, signals the rate hike scenario is off the table now that the Iran-driven energy shock is resolving, and how he frames the inflation outlook at Wednesday's press conference. May CPI, PPI, and retail sales data all drop Wednesday ahead of the decision, giving investors a full picture of the economic backdrop before the announcement.

- Asian markets were mixed on Tuesday. Japan's Nikkei 225 edged up 0.5% to breach 70,000 points for the first time ever, following the Bank of Japan's anticipated rate hike to 1% at its June 15–16 meeting — the highest level since 2008. The TOPIX slipped 0.3% as some investors rotated out of export-sensitive stocks on yen strengthening. The BOJ's move was widely expected, with probability near 100% heading into the meeting as the Iran deal's deflationary energy implications gave policymakers room to normalize.

- South Korea's KOSPI rose 1.8% on sustained gains in technology and chipmaking stocks. China's Shanghai Composite and CSI 300 were flat after weak May economic data — retail sales and fixed asset investment both contracted more than expected, with the latter reaching its weakest level since the Covid-19 crisis, though industrial production offered a slight beat on strong overseas demand.

- Australia's S&P/ASX 200 was flat as the Reserve Bank of Australia held rates at 4.35%, in line with expectations. Other regional markets were mildly positive. Investor focus across Asia remained on the upcoming formal U.S.-Iran peace deal signing this Friday in Switzerland and the pace of Strait of Hormuz reopening logistics.

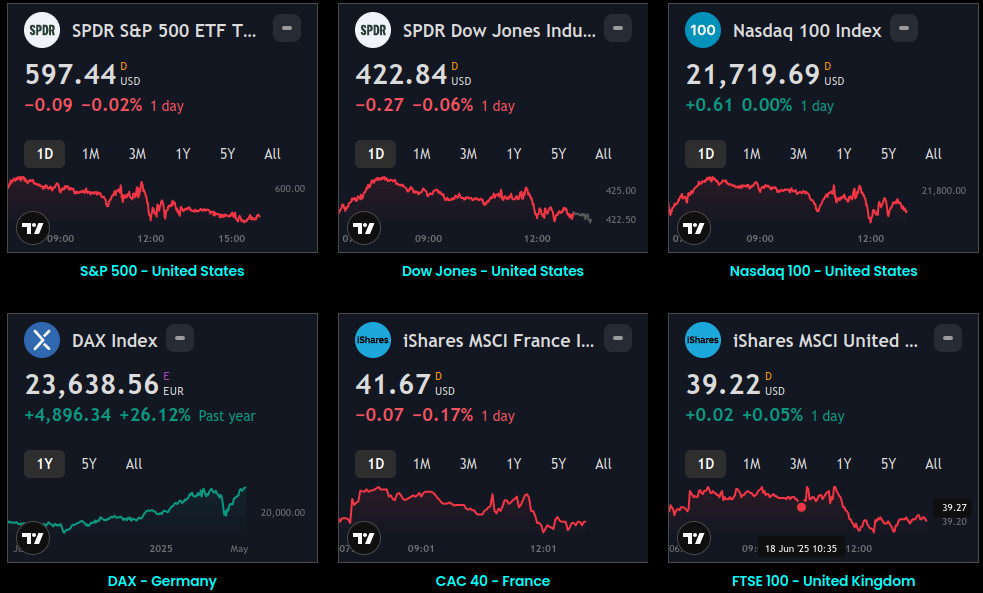

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.