US Stocks point to a slightly lower open as investors weigh renewed Iran tensions against a freshly announced 60-day peace roadmap, with all eyes turning to Thursday's PCE inflation report after last week's hawkish Fed surprise.

- S&P 500 futures traded down 0.2% to 0.3% and Nasdaq-100 futures slipped a similar amount in early Monday trading, while Dow Jones futures fell roughly 29 points, or 0.1%. Futures had pared back sharper early losses as markets digested conflicting signals out of the Middle East.

- Mediators Qatar and Pakistan announced that U.S. and Iranian officials concluded the first session of new talks with progress made on a roadmap aimed at reaching a final peace deal within 60 days. Vice President JD Vance met with Iranian officials in Switzerland for the first formal talks under the interim peace framework signed last Wednesday.

- That progress came against a more troubling backdrop: Iran said it had closed the Strait of Hormuz again over the weekend, accusing the U.S. and Israel of violating the ceasefire, while President Trump separately threatened fresh military action against Iran if Hezbollah continued attacks on Israel. The conflicting headlines — talks advancing on one hand, the Hormuz waterway shutting again on the other — are keeping volatility elevated heading into the open.

- Brent crude futures for August initially gained in Asian trading before reversing to fall 1.6% to $79.30 a barrel as the roadmap news took hold, while WTI futures for July pared an earlier 3% spike to trade about 0.8% lower near $76.

- Treasury yields remain under pressure following last week's hawkish Fed turn. The 2-year note yield hit 4.0442%, its highest since February 2025, while the 10-year climbed to 4.5048%, its highest since June 12. Traders have ramped up bets on a rate hike as soon as September, with markets now pricing roughly 75% odds of at least a 25-basis-point increase this year.

- Thursday's release of May's PCE price index — the Fed's preferred inflation gauge — is the week's central catalyst. Core PCE, which excludes food and energy, is expected to tick up from April's reading, and any upside surprise would likely reinforce the case for the rate hike markets are now bracing for.

- SpaceX (SPCX) fell more than 3% in premarket, putting it on pace for a third straight daily decline. The stock remains over 31% above its IPO price despite the recent pullback.

- In the U.K., Prime Minister Keir Starmer announced his resignation Monday morning, with nominations for a Labour leadership contest opening July 9 and Andy Burnham seen as the likely successor after a decisive special election win. Sterling slipped against the dollar on the news, while gilt yields held largely steady, having already priced in much of the political transition on Friday.

- Asian markets closed mixed Monday. Japan's Nikkei 225 jumped 1.55–1.9% to a fresh record close near 72,354, extending a run that has it up almost 8% for the prior week alone and roughly 40% year-to-date. South Korea's KOSPI gained about 0.7–2.6%, depending on the reading, closing near 9,114.55 after a week that saw it surge more than 11% on semiconductor demand.

- Hong Kong's Hang Seng slipped 0.63% in late trade, while China's CSI 300 rose sharply, up 2.39% to 5,059.66. Australia's S&P/ASX 200 was little changed, down 0.14% to 8,816.10. MSCI's broadest index of Asia-Pacific shares outside Japan added 1.0%, while Chinese blue chips traded roughly flat for most of the session before the late CSI 300 pop.

- In Europe, futures pointed to a subdued open: EUROSTOXX 50 futures eased 0.1%, DAX futures were flat, and FTSE futures edged up 0.1%, with investors there also weighing the Starmer resignation alongside the Iran headlines.

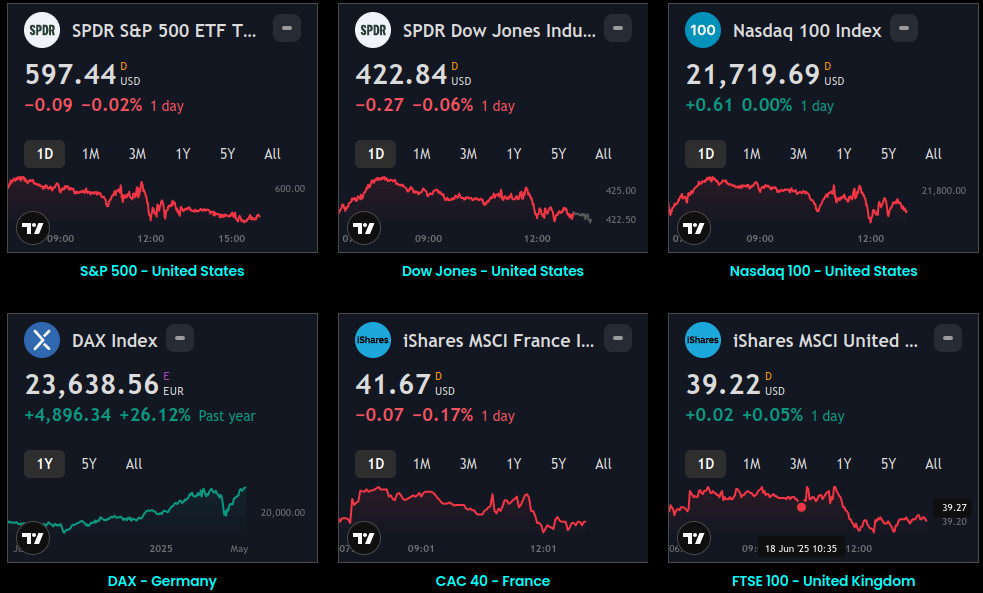

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.