- Tech stocks jumped before the bell on Thursday as blowout Micron (MU) earnings helped boost sagging confidence in the AI trade and investors counted down to the latest reading on inflation.

- Micron's record-setting quarterly results relieved Wall Street jitters over lofty AI valuations and spending. Its shares rocketed more than 18% in premarket after the company's sizeable earnings beat and stronger-than-expected outlook signaled healthy demand for its memory chips.

- Meanwhile, Qualcomm (QCOM) announced a move beyond smartphones into data center products such as chips and servers, in a bid to cash in on the AI boom. Its stock rose over 12% after it set a target of $15 billion in related new revenue.

- In another lift to spirits, oil prices fell back to levels not seen since the Iran war, down over 1% as supply flooded back through the Strait of Hormuz. Brent crude futures (BZ=F) dropped to less than $73 a barrel, while West Texas Intermediate futures (CL=F) broke below $70.

- Focus is now on the latest release of the Personal Consumption Expenditures Price Index, the Federal Reserve's preferred measure of inflation, due Thursday. The chance of interest-rate hikes this year has weighed on stocks, after consumer and wholesale prices for May came in hotter than expected. The PCE data should give investors a more complete picture of inflation for the month, amid the Iran war oil shock.

- The week's central event lands at 8:30 a.m. ET this morning: May's Personal Consumption Expenditures price index, the Fed's preferred inflation gauge. Economists polled by Dow Jones expect headline PCE to rise 0.5% month-over-month, with core PCE (excluding food and energy) seen at a faster monthly pace than April's 0.2% and a higher annual rate than April's 3.3% — a reading that would mark the highest level in roughly three years if it lands near consensus. Final Q1 GDP, May personal income data, preliminary durable goods orders, and weekly jobless claims also print this morning alongside it.

- Treasury yields ticked up slightly ahead of the data, with the 10-year note adding 1 basis point to 4.412% in early trading, as markets continue to weigh the odds of a Fed rate hike later this year following last week's hawkish dot-plot shift under new Chair Kevin Warsh.

- Oil extended its decline. Brent crude settled at $73.74 a barrel on Wednesday, its lowest level since before the U.S. and Israel first struck Iran in late February, while WTI fell to $70.34 — both having briefly touched even lower intraday levels. Crude has now fully reversed the conflict-driven spike as shipping traffic through the Strait of Hormuz gradually normalizes following the June 17 U.S.-Iran memorandum of understanding.

- Gold fell below $4,000 an ounce for the first time in seven months, last trading near $3,987–$4,002, as a tech-driven equity rally reduced safe-haven demand even amid this week's broader market volatility.

- Wednesday's U.S. session was mixed ahead of the Micron report: the S&P 500 slipped 0.10% to 7,358.22 and the Nasdaq fell 0.43% to 25,476.64, while the Dow bucked the trend, adding 182.06 points, or 0.35%, to 51,848.90. S&P Global announced Alphabet will replace Verizon in the Dow Jones Industrial Average effective at Monday's open, deepening mega-cap tech's weight in the blue-chip index.

- FedEx fell roughly 6–7% in after-hours and premarket trading despite beating both revenue ($25 billion vs. $24 billion expected) and EPS ($6.31 vs. $5.96 expected) estimates for its fiscal fourth quarter — the last report to include its freight division before that unit's spinoff as independent FedEx Freight on June 1. Citi analysts called the selloff "largely unjustified" given the operational strength.

- Asian markets rallied broadly overnight on the Micron-led chip rebound. Japan's Nikkei 225 surged 4.0–4.6% to roughly 72,366, with SoftBank up nearly 8%. South Korea's KOSPI led regional gains, jumping 5.2–5.9% to around 8,930, with Samsung Electronics up about 5.3% and SK Hynix surging 11–13%; the rally was strong enough to trigger South Korea's sidecar market-stabilization mechanism.

- Hong Kong's Hang Seng was a notable laggard, falling 1.0–1.6% on profit-taking in tech names even as the broader region rallied, though Hong Kong-listed chip names like SMIC and Hua Hong Semiconductor still gained 1.5–2.3%. China's CSI 300 rose 1.5–1.6%. Australia's S&P/ASX 200 slipped 0.3–0.7%, underperforming despite stronger-than-expected May jobs data showing unemployment easing to 4.4%. India's Nifty 50 opened 0.6% higher.

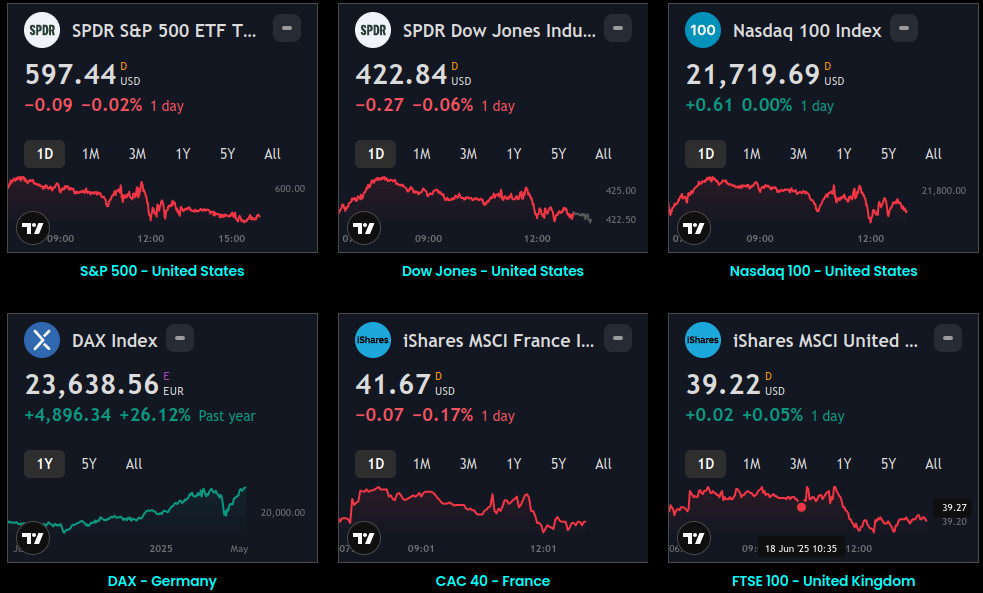

Global Indices:

Global Indices Dashboard

S&P 500 - United States Dow Jones - United States Nasdaq 100 - United States DAX - Germany CAC 40 - France FTSE 100 - United Kingdom Nikkei 225 - Japan EWH - Hong Kong Sensex - India ASX 200 - Australia MOEX - Russia MERVAL - Argentina Bovespa

Active Stocks:

Active Stocks

See the top five gaining, losing, and most active stocks for the day. It updates based on current market activity – so you’ll always see the most relevant stocks Track all markets on TradingView

Stocks, ETFs and Funds Screener:

Stocks, ETFs and Funds

Separate the wheat from the chaff – handy for sorting symbols both by fundamental and technical indicators. Sort Assets and Filter by Region, Type, Sector, Industry and Country

Forex:

Foreign Exchange Dashboard

Heatmap and Real-time quotes of selected currencies in comparison to other major currencies. Sort currencies both by fundamental and technical indicators

CryptoCurrency:

Crypto Currency Dashboard

CRYPTO HEATMAP OVERVIEW Assets by Market Capitalization

Events and Earnings Calendar:

Events & Earnings

Keep an eye on key upcoming economic events, announcements, and news. Track all markets on TradingView

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.