US Stocks fell for a fifth straight session as a renewed AI-valuation selloff gripped global markets, triggered by reports that OpenAI is leaning toward delaying its IPO, even as a cooler-than-expected PCE inflation reading and falling oil prices offered some counterbalance.

- U.S. stock futures came under pressure overnight, with the Emini S&P 500 down roughly 0.7% and the Emini Nasdaq 100 off about 1.5%, as the tech rotation that started on Wall Street earlier in the week resumed with force through the Asian session. The Roundhill Magnificent Seven ETF (MAGS), tracking Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla, slipped in premarket trading amid the broader selloff.

- The trigger was a New York Times report that ChatGPT-maker OpenAI is considering holding off on its IPO until 2027, over concerns the offering might not draw enough demand to support a roughly $1 trillion valuation. The news hit hardest at companies with direct exposure to OpenAI's fortunes, led by SoftBank Group — a major OpenAI backer — which plunged more than 12% in Tokyo trading.

- On the inflation side, Thursday's PCE price index showed prices rising at a 4.1% annual rate in May, the highest since April 2023, while core PCE (excluding food and energy) came in at 3.4% annually — both readings in line with forecasts, marking the highest core reading since October 2023. Despite the elevated levels, investors pared back expectations for further Fed rate hikes after the data landed slightly below the most bearish estimates, with Minneapolis Fed President Neel Kashkari saying Friday he now expects one rate hike this year rather than more.

- ON Semiconductor tumbled nearly 15% in premarket trading amid the broader tech-sector selloff, while Avery Dennison fell 6.1% and SanDisk dropped 5.4%. BlackBerry shares fell 3% after surging nearly 20% in the prior session, even after the company reported net income more than quadrupled in its fiscal Q1 2027 and revenue rose 25.6% to $152.9 million.

- Apple and Microsoft also weighed on sentiment after announcing price increases on consumer hardware — Apple on Mac, iPad, and home devices (15–25% hikes tied to AI chip demand) and Microsoft on the Xbox console (the 512GB model rising $100, the 1TB model $150) — both citing the ongoing memory chip shortage as a driver of higher costs passed to consumers.

- Oil extended its sharp decline. Brent crude fell roughly 4.3–4.5% and WTI dropped 3.7–4.1%, both returning to levels last seen before the Iran war began in late February, as tanker traffic resumed flowing through the Strait of Hormuz despite a reported drone or projectile attack on a Singapore-flagged cargo ship in the Gulf of Oman that forced a brief suspension of a UN-led evacuation of stranded vessels. President Trump said on Truth Social that Iran's drone strikes on transiting ships were a "foolish violation" of the ceasefire agreement.

- Iran separately reasserted its right to control shipping through the Strait of Hormuz, warning Gulf states against siding with the U.S. after Washington and six Gulf states rejected Iran's bid to charge tolls on transiting vessels — a reminder that the underlying ceasefire framework remains contested even as physical shipping flows have resumed.

- Gold rose roughly 1.1% to around $4,063–$4,092 an ounce as the in-line PCE print and broader risk-off mood lifted demand for safe havens; UBS said it sees gold recovering toward $5,200 over the next 12 months as the Fed moves toward eventual rate cuts.

- SpaceX shares fell about 1.3% to roughly $151 in premarket trading, well off the post-IPO high of $202 hit on June 16, as the stock continues to experience outsized volatility. Separately, the stock was on track for a fast-tracked addition to the Russell 1000 index after Thursday's close.

- University of Michigan's final June consumer sentiment reading is due shortly after Friday's open, with consensus at 48.9 — unchanged from the preliminary estimate and still near historic lows, though both current conditions and forward-looking expectations had shown some improvement in the preliminary report.

- Asian markets sold off sharply Friday in one of the most volatile sessions of the year. South Korea's KOSPI plunged as much as 8% intraday before closing down 5.8% at 8,411.21, triggering a Korea Exchange sidecar mechanism and a second trading halt this week alone — the index had touched a record 9,385.59 just days earlier on Monday before the violent reversal. SK Hynix fell more than 8%.

- Japan's Nikkei 225 dropped 4.2% to close at 69,360.88, with the Topix also under pressure, as SoftBank's OpenAI-linked slide dragged the broader tech-heavy index lower. Hong Kong's Hang Seng fell 1.8% to 22,671.86 and China's Shanghai Composite dropped 2.3% to 4,027.26, both hit by the same wave of global tech-sector de-risking. Australia's S&P/ASX 200 was roughly flat, up about 0.1%, a rare pocket of stability in an otherwise bruising session across the region.

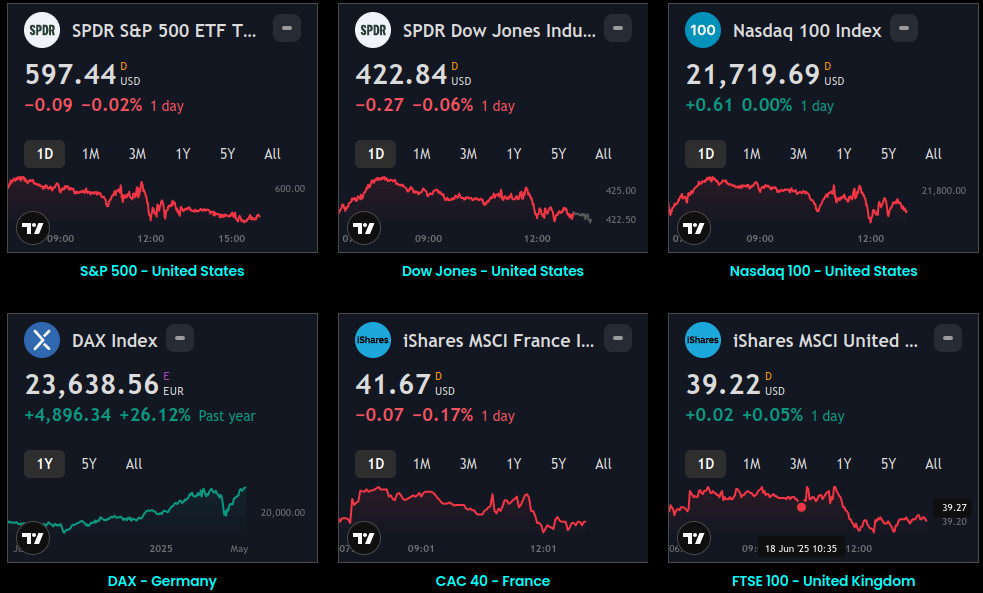

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.