US Stocks open cautiously higher after a chip-driven selloff wiped out early gains in Wednesday's session, with all eyes now on the June nonfarm payrolls report at 8:30 a.m. ET — the last major data print before Friday's market closure for Independence Day.

- U.S. stock futures edged up 0.2% ahead of the open after all three major averages ended Wednesday's session lower, with the Dow erasing a 423-point intraday gain to close just below the flatline, the S&P 500 slipping 0.2%, and the Nasdaq Composite sliding 0.7% as investors aggressively rotated out of chipmakers following a blockbuster Q2 for the sector. Wall Street futures tipped back into the green overnight on signs of progress in Iran talks and a key Warsh comment on rates.

- The June nonfarm payrolls report drops at 8:30 a.m. ET, moved a day early from its usual Friday slot due to Friday's Independence Day holiday. Economists polled by Dow Jones expect 115,000 jobs added in June, a notable step down from May's stronger-than-expected print, reflecting a labor market that has been in a low-hire, low-fire mode for several months. Wednesday's ADP National Employment Report showed private sector payrolls grew by only 98,000 in June — modestly below consensus — offering a cautious setup for the official number. June factory orders also print at 10:00 a.m. ET.

- Federal Reserve Chair Kevin Warsh made his most notable public comments since his hawkish debut FOMC meeting, telling an audience Wednesday that inflation expectations had eased over the past month and signaling there was no urgency to raise interest rates — a meaningful dovish tilt from his prior stance that rattled markets on June 17. The comments, delivered just as the market opened, helped partially stabilize stocks midday before the afternoon chip selloff resumed.

- Micron Technology (MU) dived more than 10% Wednesday despite its stunning 260% year-to-date gain through Q2, as investors took profits on stretched valuations. SanDisk (SNDK) shed over 10% in the same session, while Nvidia and Broadcom fell between 1% and 2%. The VanEck Semiconductor ETF (SMH) posted one of its worst single-day performances since April 2025.

- Meta Platforms (META) jumped nearly 9% in premarket Thursday on reports the company is building a cloud business to sell excess AI computing capacity to enterprise customers — a direct move into the hyperscaler market currently dominated by Amazon Web Services, Microsoft Azure, and Google Cloud. The move would represent a significant strategic expansion for Meta beyond its core advertising business.

- Apple (AAPL) is in active talks to source memory chips from ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC), both on the Pentagon's Section 1260H entity list, with any supply earmarked primarily for the Chinese domestic market. No final agreement has been reached. Separately, Nikkei Asia reported Apple is planning a five-model iPhone lineup split across H2 2026 and H1 2027, including a larger-than-expected volume of folding handsets.

- KNDS, the Franco-German tank maker behind the Leopard and Leclerc, postponed its highly anticipated Paris and Frankfurt dual-listing, citing current market volatility in the European defense sector. The company had been targeting a valuation of more than €12 billion but struggled to build sufficient investor support at that level. President Trump separately disclosed he is pushing for a 15–20% minimum tariff on all EU goods, sending the euro lower and weighing on European futures.

- Oil hit new four-month lows overnight. Brent crude fell 1.0% to $70.88 a barrel — back to pre-Iran war levels — as Trump said talks with Iran had gone well in Qatar and more oil tankers transited through the Strait of Hormuz. WTI settled below $70 for the second time this week. Gold bounced 0.7% to $4,059 an ounce after tumbling 14% in Q2, with the recovery supported by softer jobs data and the Warsh rate-hike pullback. The Japanese yen hit a fresh 40-year low of 162.84 against the dollar Wednesday, prompting intervention warnings from Tokyo's Ministry of Finance, though prior interventions in April and May proved short-lived despite nearly 12 trillion yen deployed.

- Asian markets extended their tech-driven declines sharply on Thursday. South Korea's KOSPI bore the full brunt, tumbling as much as 6% in early trade and triggering a sidecar circuit breaker before closing down 4.8%, extending Wednesday's 2% slide — a combined two-day drop of nearly 7% on top of the 68% surge the index posted in Q2 alone. Samsung Electronics closed 9.1% lower and SK Hynix dropped 14.6%, with SK Square, SK Hynix's largest shareholder, falling more than 10%. Kioxia Holdings in Tokyo fell 11.4%, while Tokyo Electron dropped 6.2% and Advantest slid 6.7%.

- Japan's Nikkei 225 fell roughly 2% to around 69,000, snapping a three-day winning streak as chip and AI-related stocks led declines. Financial and consumer names offered some cushion — Mitsubishi UFJ gained 1.9%, Mizuho Financial added 2.4%, and Toyota rose 3.6% — but not enough to offset the semiconductor drag. Hong Kong's Hang Seng bucked the regional trend, gaining 0.9% on its first session back after a holiday, buoyed by strength in local tech, biopharma, and auto names. China's mainland indexes stayed in the red alongside the broader risk-off tape. Australia's S&P/ASX 200 and MSCI's broadest index of Asia-Pacific shares outside Japan both fell, with the MSCI index off 1.2%.

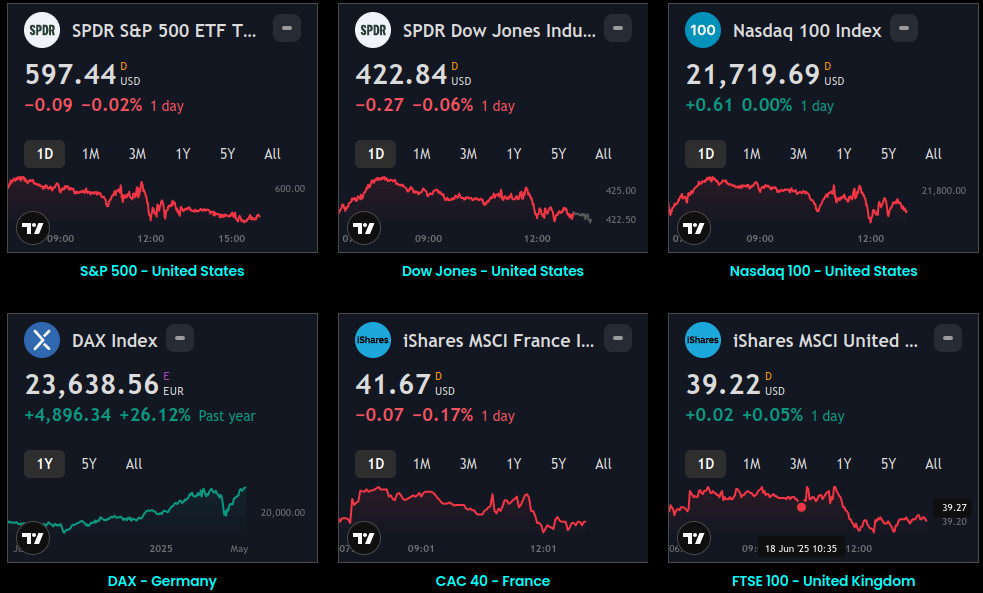

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.