US Stocks open the second half of 2026 on a cautious note as Iran rules out direct talks with U.S. officials in Doha, pushing oil back below $70, while Nike's miss after the bell weighs on consumer sentiment and a heavy data calendar — headlined by ISM Manufacturing and a Fed Chair speech — keeps markets on edge to start Q3.

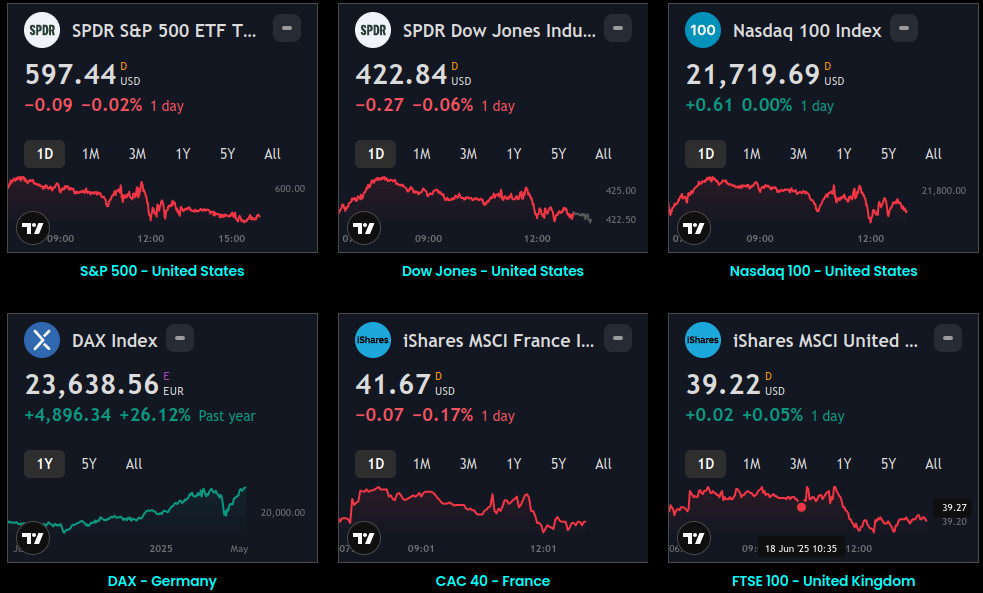

- U.S. stock futures slipped modestly at the open, with S&P 500 futures down 0.2%, Nasdaq 100 futures off 0.3%, DAX futures lower 0.1%, and FTSE futures down 0.3%, as Iran's refusal to engage in direct talks with U.S. delegates in Doha dampened the risk-on mood that had lifted all three major indexes to fresh records at the end of Q2. The Roundhill Magnificent Seven ETF (MAGS) gained a modest 0.16% in early premarket as the broader tape was uncertain.

- Q2 2026 closed Tuesday as the best quarter for the S&P 500 and Nasdaq in six years, despite the Iran war. The S&P 500 wrapped the first half up roughly 15% year-to-date, while the Nasdaq has gained north of 20% and the Dow posted its best quarter since 2022. Micron Technology's 400% first-half gain was the headline single-stock story of the period, officially placing the chipmaker inside the S&P 500's top 10 constituents.

- Iran dealt a blow to peace talks Tuesday, stating it would not meet directly with U.S. delegates in Doha and rejecting the format Washington had proposed. Iranian and U.S. officials did resume indirect negotiations via Qatar and Pakistan as intermediaries, Reuters reported, but Tehran's refusal to sit across the table from American diplomats underscored how fragile the ceasefire framework remains. Oil fell on the news, with WTI crude sliding 1.1% to $68.77 per barrel — the lowest settlement since before the war began — and Brent slipping 1.0% to $72.20.

- Nike (NKE) fell 3.5% in premarket after reporting fiscal Q4 results after Tuesday's close. The company beat earnings estimates but CEO Elliott Hill said there had been "nothing normal" about the retail landscape during the quarter, and the stock's reaction reflected disappointment over continued China weakness and a multi-year turnaround that is proving slower than investors had hoped. JPMorgan had already cut its Nike price target to $47 ahead of the report.

- SpaceX (SPCX) gained 2.0% to $174.32 in premarket after Wedbush Securities initiated coverage with an Outperform rating and a $190 price target. Analyst Dan Ives called SpaceX "one of the most differentiated assets within the tech market," with Starlink driving connectivity, Starship creating a demand flywheel, and the Colossus AI cluster generating accelerating deal flow across enterprise customers.

- Kroger (KR) fell 2.8% in premarket after announcing a $1.65 billion acquisition of supermarket operator Giant Eagle — $1.25 billion in cash plus assumption of roughly $400 million in liabilities — as the grocery chain seeks scale following its failed $25 billion merger attempt with Albertsons, which regulators blocked in 2024. Analysts noted the deal faces a tougher competitive backdrop with Walmart and Amazon continuing to expand grocery market share.

- Bloom Energy (BE) jumped 8.0% after expanding its strategic partnership with Brookfield, increasing a financing framework for power projects from $5 billion to $25 billion, with the focus on AI infrastructure and data center power needs. Alcoa (AA) tumbled 4.1% after saying its $4.1 billion acquisition of South32 mines is expected to have an immediate dilutive effect on earnings per share and free cash flow upon closing.

- FMC Corp. (FMC) surged 8.3% in premarket, General Mills (GIS) rose 4.4% ahead of its Wednesday morning earnings report, and ServiceNow (NOW) gained 4.1%. Essex Property Trust (ESS) tumbled 11.6%, while Public Storage (PSA) fell 4.1% and Universal Health Services (UHS) dropped 4%.

- The economic calendar is front-loaded with market-moving data. June's S&P flash U.S. Manufacturing PMI prints at 9:45 a.m. ET, followed at 10:00 a.m. by the June ISM Manufacturing PMI and May construction spending. The ISM print will be closely watched given that PMIs across Asia came in broadly disappointing Wednesday morning, with contraction readings in China, Indonesia, South Korea, Taiwan, and Vietnam — China's data was particularly hurt by weak new export orders, raising questions about whether a Q3 demand slowdown is beginning to take shape globally.

- Fed Chair Kevin Warsh is scheduled to speak during the New York morning session, his first public remarks since delivering the hawkish dot plot at his debut FOMC meeting on June 17. Markets will be parsing every word for any softening — or hardening — of his rate outlook now that oil has rolled below $70, which meaningfully changes the inflation calculus that led nine of 18 officials to pencil in at least one hike this year. CME FedWatch shows a 70.6% probability of no change at the July meeting.

- Gold fell 0.9% to around $3,974–$4,003 an ounce and silver dropped 2.4% to $58.47, both under pressure from mild dollar strength and fading safe-haven demand as oil eased. Bitcoin slipped 1.3% to around $58,545.

- Asian markets closed mixed on Wednesday to open Q3. Japan's Nikkei 225 rose 0.8%, supported by a strong Q2 Tankan survey in which large manufacturers reported their highest confidence reading since March 2018, and Japan's June Manufacturing PMI confirmed a fifth straight month of expansion at 54.8. India's Nifty 50 also edged higher, with India's June Manufacturing PMI posting its 60th consecutive month of expansion at 54.2. South Korea's KOSPI fell 1.5–2.4% to around 8,274, continuing a volatile start to the new quarter with KOSPI chip names under pressure from the disappointing regional PMI data. Hong Kong's Hang Seng fell 0.6%, China's Shanghai Composite gained 0.9%, and Australia's S&P/ASX 200 fell 0.6% on the weak regional PMI backdrop. The TAIEX in Taiwan bucked the trend, rising 2.5%.

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

6No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.