- Tech is calling the tune this Monday as Nasdaq futures surge more than 1% post-holiday, chipmakers rebound, and Wall Street braces for the week's first major data catalyst with ISM Services due at 10 a.m. ET.

- S&P 500 futures are up 36 points, or +0.48%, to 7,564; Dow futures add just 33 points, or +0.06%, to 53,216; Nasdaq futures lead all comers, climbing 310.50 points, or +1.05%, to 29,866 as traders return from the three-day Independence Day weekend. The Russell 2000 futures add a modest +0.14%, keeping small-caps in a supporting role on the day.

- The VanEck Semiconductor ETF (SMH) is up 2.4% ahead of the opening bell as chip stocks rebound after Thursday's tech-driven drag; the Roundhill Magnificent Seven ETF (MAGS) adds 0.54% to $65.37 in premarket, with the basket of GOOG, AMZN, AAPL, META, MSFT, NVDA, and TSLA broadly firmer.

- Vera Therapeutics (VERA) jumps 9% in premarket as investors position ahead of Tuesday's high-stakes FDA PDUFA decision on atacicept for IgA nephropathy; the FDA assigned the July 7, 2026 target action date under Priority Review after the BLA was submitted via the Accelerated Approval Program. Meta Platforms (META) adds 1.4% in pre-open trading, attempting to recover from last Thursday's steep sell-off.

- Novartis (NVS) is a story name in premarket after agreeing to pay up to $1.5 billion for Myricx Bio to bolster its oncology portfolio, with $1.1 billion due upfront and up to $400 million in additional milestone payments. Clarivate (CLVT) announced a definitive agreement to divest its Life Sciences & Healthcare segment to Altaris for $600 million and reaffirmed its full-year outlook.

- SpaceX (SPCX) is the index story of the session: passive fund managers are required to buy the stock today ahead of its official Nasdaq-100 addition before Tuesday's open; the QQQ alone could absorb up to $4.3 billion worth of SPCX, with total Nasdaq-100 tracking funds potentially buying up to $27 billion into a public float of only 3%–5% of all outstanding shares. SPCX traded most recently near $162 and remains 22% below its post-IPO peak.

- SK Hynix (SKHY) confirmed today it will raise 43 trillion KRW (~$28.1 billion) via a U.S. Depositary Receipt listing, with trading expected to begin on the Nasdaq Global Select Market on Friday July 10; the deal would be the largest-ever first-time share sale by a foreign company in U.S. history, eclipsing Alibaba's $21.8 billion debut in 2014.

- On the macro calendar today: ISM Non-Manufacturing Composite for June prints at 10:00 a.m. ET, offering a read on service-sector momentum after June nonfarm payrolls came in at just 57,000, roughly half the consensus estimate of 113,000; the fed funds rate sits at 3.63% and markets have dialed back rate-hike conviction. This week's marquee event is the release of FOMC minutes from the June meeting on Wednesday, July 8 — the first under Chair Kevin Warsh, who declined to participate in the quarterly dot plot.

- In commodities, WTI crude August futures trade at $68.46/bbl, off -0.33%, consolidating after an intraday surge to $69.26 earlier in the Asian session; the Strait of Hormuz resumption and OPEC production increases continue to cap the rebound. Gold futures are up +0.83% to $4,159.90/oz, holding near multi-week highs, while Bitcoin (BTC-USD) is flat at $62,830, trading just below the $63,914 Asian session high reached overnight in what has been a five-day winning streak from a $58,000 base.

- Japan's Nikkei 225 closed down -1.18% to 68,919 and the broader SSE Composite shed -0.54% to 4,021 as Asian chipmakers saw a sharp rotation; the Hang Seng rose +266 points to 23,616, while Shenzhen's index dropped -1.38% to 15,383. The Shanghai Composite closed at 4,021, essentially flat for the session.

- South Korea's KOSPI surged +5.76% to 8,088 — the standout performer in the region — as the SK Hynix U.S. listing frenzy lifted sentiment across the memory chip complex; the S&P/ASX 200 in Sydney closed +1.37% to 8,844, leading developed-market Pacific gains and outperforming the subdued Japanese tape decisively.

- Taiwan's TAIEX closed at 46,780, up +0.08%, a mild session as the index holds near multi-year highs; Singapore's STI remains in a technically rising trend channel. India's S&P BSE SENSEX added +0.34% to 77,763, with the Nifty 50 testing near-term technical resistance around 24,340 where a sustained break would signal a push toward 25,260.

US Stocks open cautiously higher after a chip-driven selloff wiped out early gains in Wednesday's session, with all eyes now on the June nonfarm payrolls report at 8:30 a.m. ET — the last major data print before Friday's market closure for Independence Day.

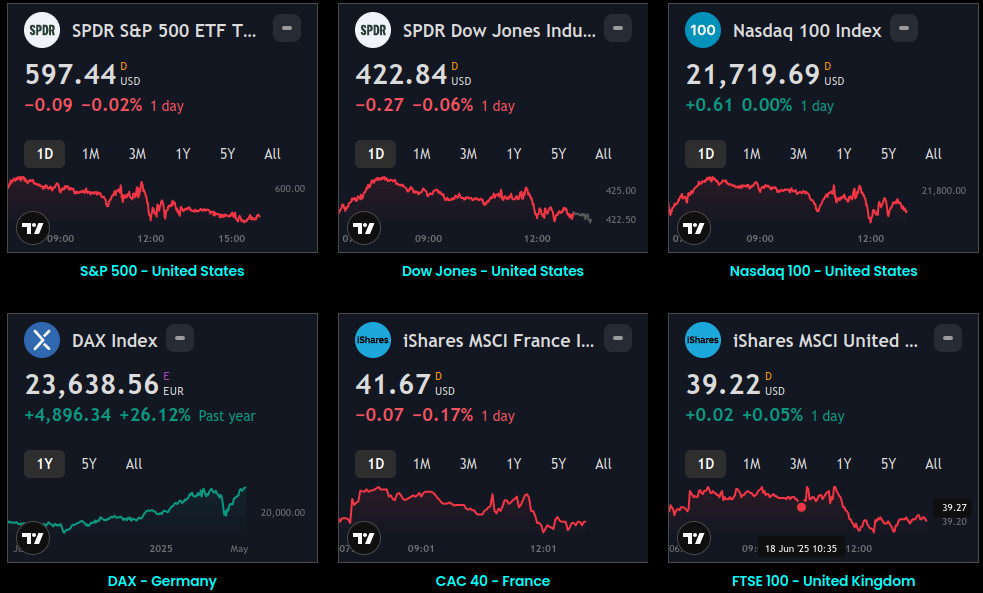

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.