A Seoul circuit breaker, a sell-the-news Samsung rout, and a fresh AI valuation reassessment are colliding with SpaceX's Nasdaq-100 debut to set up a split tape on Wall Street Tuesday.

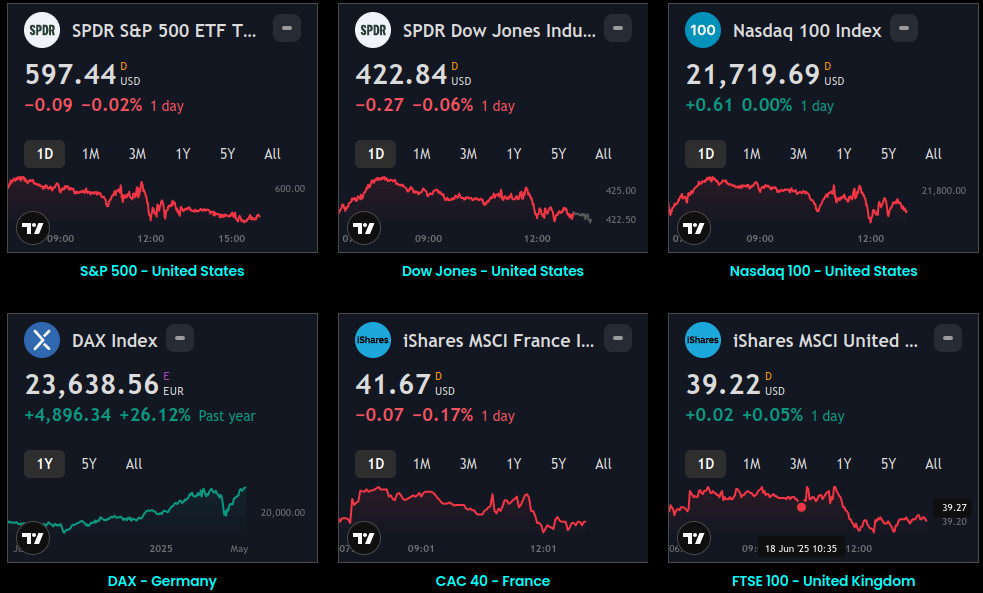

- Nasdaq-100 futures are leading the premarket selloff, falling 0.9%, while S&P 500 futures are down 0.1% and Dow Jones futures are edging higher by 87 points, or 0.2%, as investors rotate out of artificial intelligence names for a second straight session.

- In premarket individual movers, Fiserv (FISV) is the standout gainer, surging 7.53%, followed by Baxter International (BAX) +2.32% and CME Group (CME) +2.15%.

- FISV is expected to announce its fiscal Q2 2026 earnings imminently; the Street is modeling $1.91 per share diluted EPS, down 22.7% year-over-year from $2.47 in the year-ago quarter.

- Micron Technology (MU) is trading 5.7% lower in premarket at $929, unable to hold post-earnings gains from its record fiscal Q3 2026 results, having shed more than a fifth of its value since peaking near $1,255 in late June in a classic sell-the-news dynamic.

- KLA, Marvell Technology (MRVL), Nvidia (NVDA), Broadcom (AVGO), and AMD are all posting premarket declines alongside MU in a broad chip-sector retreat.

- SpaceX is officially joining the Nasdaq-100 before Tuesday's open, with index-tracking funds and ETF sponsors having begun purchasing shares after Monday's close.

- SpaceX is shedding about 2% in premarket ahead of its Nasdaq-100 entrance, a counterintuitive move as passive-buying demand is offset by the same AI-rotation sentiment weighing on the broader tech complex.

- WTI crude oil rose to $69.31 per barrel on July 7, up 1.10% from the prior session, though the commodity has fallen 24.09% over the past month as post-conflict supply normalization accelerates.

- Reports indicate at least eight Japan-linked vessels exited the Strait of Hormuz including five supertankers, while Saudi Aramco cut its Arab Light crude price for Asian buyers by $11 per barrel, widening the discount to $1.50 below the regional benchmark.

- Gold is trading at $4,159.90, up $34.20 or +0.83%, while Bitcoin (BTC-USD) is at $62,830.37, down just 0.04%, and Crude Oil Aug 26 futures are at $68.46, off 0.23%.

- The VIX is ticking higher to 16.34, up 3.35%, reflecting the renewed skittishness in tech-heavy positioning.

- Shell raised its Q2 2026 integrated gas production guidance to a range of 610,000–650,000 barrels of oil equivalent per day, up from the prior 580,000–640,000 guide, ahead of its full Q2 earnings release scheduled for July 30.

- The upgraded range still marks a notable decline from the 909,000 barrels produced in Q1, which Shell attributed to the impact of the Middle East conflict on Qatari volumes.

- Tokyo's Nikkei 225 closed down 2.1% to 68,256.96, dragged by chip-equipment maker Tokyo Electron (-3.9%) and Kioxia Holdings (-11.3%).

- The broader TOPIX had closed the prior session at 4,101.96, a record high, but Tuesday's chip-led reversal erased that momentum.

- South Korea's KOSPI closed at 7,656.31, down 395 points or 4.91%, after opening 1.64% lower and plunging more than 8% at its nadir, triggering a circuit breaker that halted trading for 20 minutes.

- The decline was driven by heavy profit-taking in Samsung Electronics despite a record Q2 operating profit of 89.4 trillion won ($58.5 billion), which surpassed the market consensus of 85 trillion won.

- The Kosdaq fell 15.84 points, or 1.87%, to close at 831.23.

- The Hang Seng in Hong Kong declined 0.7% to 23,444.20, while the Shanghai Composite gave up 1.3% to 3,990.25.

- Taiwan's Taiex lost 2.3%, with heavy selling concentrated in TSMC and downstream chip-supply-chain names mirroring the Seoul rout.

- Australia's S&P/ASX 200 declined 0.3% to 8,803.90, while India's Sensex rose 0.5%' , making the Nifty 50 area one of the few constructive pockets across the Asia-Pacific session as defensive and domestic-demand stocks outperformed amid the regional tech exodus.

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.