- Global markets are attempting to claw back from a geopolitical risk-off shock as US equity futures stabilized overnight after Washington confirmed a second straight day of strikes on Iran, throwing the Strait of Hormuz back into focus and forcing traders to price oil, rates, and risk simultaneously.

- US index futures climbed in the overnight session late Wednesday, reversing an earlier sell-off triggered by the Iran escalation: Nasdaq 100 futures rose 0.19%, S&P 500 futures climbed 0.08%, and Dow futures added 0.10%. Wednesday's cash close left the Dow at 52,348, the S&P 500 at 7,482 (-0.28%), and the Nasdaq Composite at 25,871 (+0.20%), with the VIX sitting at 16.88.

- Oil pulled back from its geopolitical spike: Brent crude eased to $77.86 a barrel after jumping 5.2% to settle at $78.02 on Wednesday, while WTI August futures dipped 0.20% to $73.37 a barrel after closing Wednesday at $73.52, its biggest single-session gain since June 1. Both benchmarks had hit their highest levels since June 22 on Wednesday before paring.

- Gold extended its slide to around $4,030 an ounce on Wednesday, touching its lowest level since July 2 after Trump declared the Iran interim peace deal "over," while Fed minutes from the June meeting showed only a few policymakers favored an immediate rate increase, though officials expressed growing concern about inflation. Markets continue to price in at least one Fed rate hike by end-2026, a headwind for gold.

- Bitcoin (BTC-USD) dropped 2.40% to $62,128, tracking risk-off flows as elevated oil prices stoked inflation fears, while crude oil futures surged 5.48% on the same day, underscoring the continued inverse relationship between energy supply disruption and crypto liquidity.

- The marquee earnings event today is PepsiCo (PEP), reporting Q2 2026 before the open with the Street expecting EPS of $2.21 on revenue of $23.96 billion. PEP stock has been mostly flat year-to-date due to weaker North American snack sales, and options traders are pricing in a 4.14% move in either direction post-print.

- Key watch items in the PEP print include pricing power on Frito-Lay products after PepsiCo cut prices by up to 15% on popular snack brands earlier this year under pressure from activist investor Elliott Investment Management, which urged management to simplify operations and revive snack volume growth.

- Arista Networks (ANET) closed at an all-time high of $181.05 Wednesday, up nearly 9%, as AI-driven demand for data center networking infrastructure continued to boost investor optimism. The Nasdaq Composite's modest positive close amid the broader Iran-driven sell-off was almost entirely attributable to outperformance in ANET and a handful of AI infrastructure names.

- June existing home sales data are due today, the key US macro print on the calendar alongside the PEP earnings release.

- The 10-year Treasury yield sat at 4.579%, keeping pressure on rate-sensitive sectors heading into the open, with the Fed's neutral-to-hawkish tilt from Wednesday's FOMC minutes still fresh in bond market positioning.

- Japan's Nikkei 225 closed Thursday up +1.55%, with the index rising to approximately 67,832 in morning trade as AI-related shares fuelled optimism; semiconductor names anchored the rebound, with flash memory chipmaker Kioxia jumping 9.4% and chip equipment maker Advantest surging 6.4%. The broader TOPIX rose 0.2% to approximately 4,015 as gains were concentrated in tech rather than spreading broadly to domestic cyclicals.

- South Korea's KOSPI closed Thursday up 0.62% to 7,291.91, recovering modestly from a multi-week low, after reports that SK Hynix's planned US ADR offering was more than seven times oversubscribed. SK Hynix surged 5.83% and Samsung Electronics edged up 0.36% after suffering sharp losses the prior session; the secondary Kosdaq closed up 1.15% to 794.00.

- Hong Kong's Hang Seng Index fell 0.7%, or 169 points, to close at 24,030 on Thursday, reversing early gains as technology volatility weighed: Zhipu AI surged 11.3% as lock-up expiry fears eased, but MiniMax slumped nearly 18% during its first major lock-up expiry, while Tencent shed 1.9%, Meituan fell 3.0%, and Kuaishou dropped 4.3%.

- Mainland China's Shanghai Composite gained 1.66% to close at 4,037, led by China Merchants Securities (+7.13%), Sanan Optoelectronics (+5.95%), and Jiangsu Hengrui (+2.61%); technology stocks including Zhongji Innolight (+3.3%) and NAURA Technology (+2.7%) also advanced, while the CSI 300 edged down to 4,751 — its lowest since June — diverging from the Composite's gains.

- Australia's S&P/ASX 200 slipped 0.26% to close at 8,762.5, extending its fourth consecutive session of losses as the Iran escalation and elevated oil prices pressured miners and the broader index; energy stocks provided some offset, but materials and financials remained soft.

- India's Nifty 50 closed Wednesday at 23,882, down 2.12%, its steepest single-session drop in three months, after Trump declared the Iran ceasefire over; the Sensex fell 2.15% to 76,504. Indian shares are expected to open modestly higher Thursday as Nifty 50 futures signal a partial recovery, with TCS Q1 FY27 results the domestic catalyst of the session.

- Singapore's STI Index closed Wednesday at 5,401.95, up 1.12%, one of the few regional outperformers as confidence in Singapore banks supported the index. Taiwan's TAIEX closed at 45,354.61, off 0.83%, as the chip-sector volatility rippling from KOSPI and Nikkei continued to weigh on the island's semiconductor-heavy benchmark.

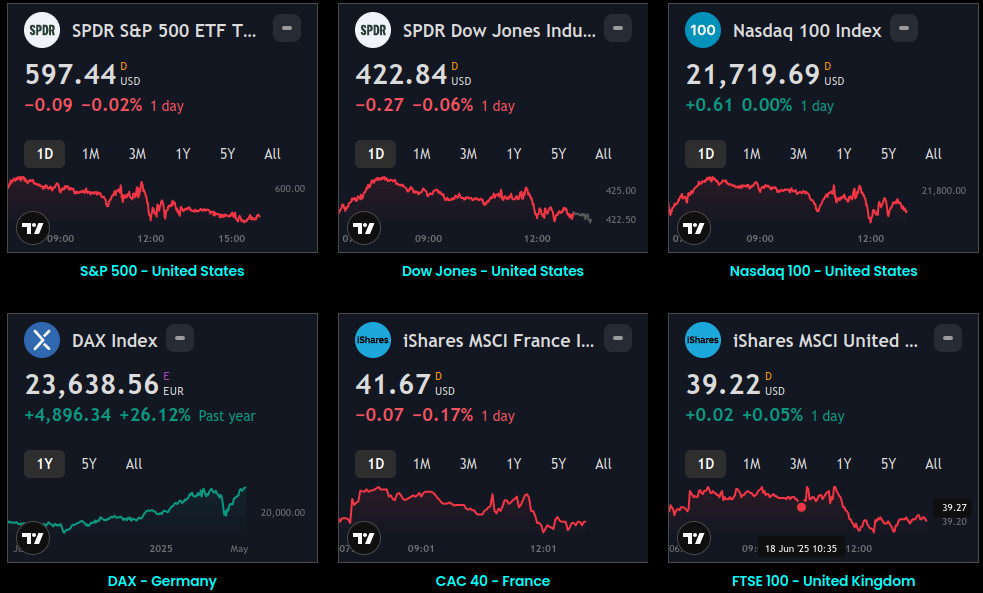

Global Indices:

Global Indices Dashboard

S&P 500 - United States Dow Jones - United States Nasdaq 100 - United States DAX - Germany CAC 40 - France FTSE 100 - United Kingdom Nikkei 225 - Japan EWH - Hong Kong Sensex - India ASX 200 - Australia MOEX - Russia MERVAL - Argentina Bovespa

Active Stocks:

Active Stocks

See the top five gaining, losing, and most active stocks for the day. It updates based on current market activity – so you’ll always see the most relevant stocks Track all markets on TradingView

Stocks, ETFs and Funds Screener:

Stocks, ETFs and Funds

Separate the wheat from the chaff – handy for sorting symbols both by fundamental and technical indicators. Sort Assets and Filter by Region, Type, Sector, Industry and Country

Forex:

Foreign Exchange Dashboard

Heatmap and Real-time quotes of selected currencies in comparison to other major currencies. Sort currencies both by fundamental and technical indicators

CryptoCurrency:

Crypto Currency Dashboard

CRYPTO HEATMAP OVERVIEW Assets by Market Capitalization

Events and Earnings Calendar:

Events & Earnings

Keep an eye on key upcoming economic events, announcements, and news. Track all markets on TradingView

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.